Sellers costs outlined before you sell your home can help you understand that it doesn’t just mean collecting a check at closing. While the sale can be financially rewarding, there are also expenses sellers should plan for before and during the process. Understanding these costs ahead of time helps you set realistic expectations and avoid surprises.

Many seller expenses begin before the home ever goes on the market. You may choose to invest in repairs, cosmetic updates or professional staging to make the home more appealing to buyers. Some sellers purchase a home warranty for the buyer as an added incentive, covering major systems for the first year. Don’t forget moving expenses: hiring movers, renting a truck or paying for temporary storage.

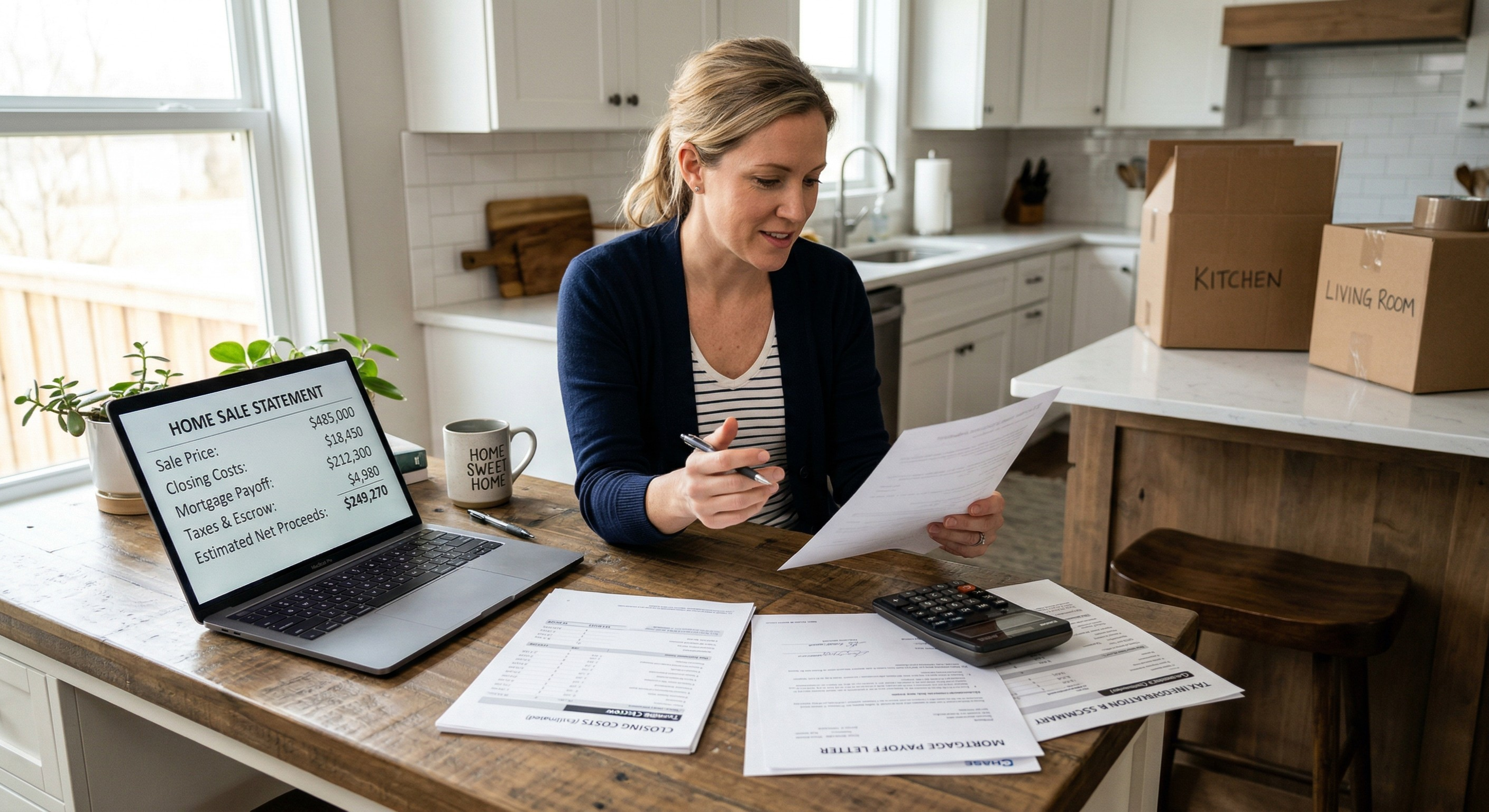

At closing, sellers are responsible for property taxes up to the date of sale, prorated based on how long you owned the home that year. You may owe capital gains taxes, depending on your individual situation and how long you lived in the property. You’ll also pay off the remaining balance of your mortgage, which may differ slightly from your last statement due to accrued interest. Sometimes, sellers may cover the cost of a title insurance policy for the buyer.

Another major expense is real estate commission. This is typically a percentage of the final sale price and is split between the listing agent and the buyer’s agent. In return, agents handle pricing strategy, marketing, negotiations and paperwork, helping the transaction move smoothly from listing to closing.